There are moments in markets when the tone shifts from scepticism to optimism and then on to exuberance. Investors stop asking what can go wrong and start asking how far it can go. We are not necessarily at the end of that process, but we are clearly well into the optimism phase.

The AI trade is the dominant force in global equity markets. Concerns around oil prices, inflation, higher interest rates, larger government deficits and geopolitics have only increased in recent months, but for now they are overshadowed by the AI investment boom. The market has chosen to focus on growth over risk, optimism over doubt and the future over the present.

There are plenty of signs that sentiment has become stretched. AI-related stocks have seen extraordinary moves over very short periods. ARM, the chip designer, and DELL, the computer manufacturer, both rose around 100% in less than ten trading days in May. Intel (INTC) has almost tripled in the last two months, while Sanddisk (SNDK) is up more than 600% year to date. Marvell Technology (MVRL), a semiconductor company, is up more than 250% year to date and added 32% in a single day after Nvidia’s CEO Jensen Huang suggested it could soon join the “trillion-dollar club”. In normal markets, moves like these would look almost absurd.

The point is not that every move is irrational. We have partly benefited from these same dynamics in some of our long positions, but in all the cases we can comfortably justify the fundamental rational. We bought Micron (MU) in September last year, and the stock is now up roughly 700% in about eight months. We also owned Bloom Energy (BE) from around USD 18-20 per share to USD 165-170, a move that took place in less than a year. Since then, Bloom has risen further to around USD 300 per share, equivalent to roughly 1,200% since the start of 2025.

These were not random moves in random companies. Micron has benefited from being one of three key suppliers of DRAM and HBM memory, crucial for further data centre build out. The incremental buyer of memory chips is no longer price-sensitive PC manufacturers, but rather price insensitive hyperscalers. We believe the current memory cycle will last longer than any memory cycle in the past.

Bloom has won some massive contracts and so far, executed well. It sits at the centre of the “behind-the-meter” power debate, where speed of deployment, grid constraints and the need for reliable on-site power have become increasingly important. These are exactly the kinds of bottlenecks we have written about for a long time, for instance in October 2025 – “Bring Your Own Power – How the Data Center is Rewiring the Grid”.

However, there is a difference between a fundamentally attractive set-up and a valuation that leaves no room for disappointment. We still own Micron, although recently trimmed the position, as the stock has rerated from about 4x to 10x 2027 P/E despite extraordinary earnings upgrades. We sold Bloom as the valuation became increasingly difficult to justify, and it has only become more demanding since. That does not mean the underlying thesis is wrong. It simply means that price eventually matters, even when the underlying opportunity is very strong.

There is no doubt that AI demand is real. Hyperscaler capex is real. The need for compute, memory, networking, power, cooling and grid infrastructure is real. However, bubbles rarely form around things that are completely fake. They usually form around something important, where the underlying thesis is right, but where expectations, positioning and price action eventually run ahead of what can reasonably be delivered.

That is the environment we are increasingly trying to navigate. It is not that some companies simply look fundamentally expensive, that is almost always true somewhere. The more important issue is that price action is disconnecting from fundamentals and is becoming increasingly dominated by momentum, retail activity, options flows and the fear of missing out.

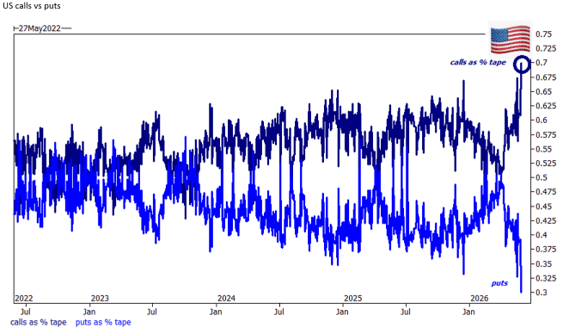

When everyone wants calls, risk management matters

Source: Goldman Sachs

This chart on US calls versus puts captures the mood quite well. Call activity has risen sharply as a share of total option activity, while put demand has collapsed. In plain English, investors are increasingly positioned for upside, not protection.

This matters. In normal markets, overvaluation is a reason to be short. However, in markets like this, overvaluation can become a reason why a stock goes up even more, because the higher it goes, the more attention it attracts from retail flows and momentum-oriented capital. “Pigs really can fly” for a while in this type of environment. Over the recent quarters, we have suffered from this dynamic in some short positions that we would argue have no, or only tangential, exposure to AI data centres or power. While we remain confident in our fundamental analysis and valuation work, the positions became impossible to hold as they caught the eye of retail investors hunting momentum stocks.

The current market environment is simply treacherous and that is why we reduced gross exposure during the month, on both the long and the short side. This is not a signal that we are less convinced about our long-term themes, nor that we no longer see attractive shorts. It is rather a recognition that the volatility of outcomes has increased and that near-term risk-reward has deteriorated. Put differently, when upside volatility becomes this extreme, the risk of being fundamentally right but tactically too early rises materially.

Importantly, we have not stepped away from the market. We remain invested in the areas where we believe the structural opportunity is strongest. What we have done is to reduce some of the most volatile positions on both sides of the book. On the long side, that means trimming names where expectations and price action had moved very quickly. On the short side, it means reducing exposure to companies where the fundamental case may still be valid, but where the near-term risk of retail-driven upside volatility had become too high.

We believe this gives us a better risk profile. It reduces the probability that short-term volatility dominates the portfolio, while still leaving us with meaningful exposure to the themes we believe in. It also provides us with more flexibility to be aggressive when this dynamic eventually fades. Retail-driven momentum, call buying and speculative positioning can dominate for periods, but they do not repeal gravity. Eventually, companies still need to deliver earnings, returns on capital and cash flow that justify their valuations. The challenge is timing since being “right” too early in a market like this can be very expensive, and in practice, indistinguishable from being wrong.

- Portföljförvaltare och grundare av fonden Coeli Energy Opportunities.

- Mer än 15 års erfarenhet av investeringar från både publika och private equity-sidan.

- Förvaltade fonden Coeli Energy Transition under perioden 2019 - 2023.

- Spenderade sex år på Horizon Asset i London, en marknadsneutral hedgefond.

- Började arbeta tillsammans med Vidar Kalvoy 2012.

- Fem år inom Private Equity på Morgan Stanley.

- Startade sin investeringskarriär inom tekniksektorn på Sweden Robur i Stockholm 2006.

- Utbildad Civilingenjör från Kungliga Tekniska Högskolan.

- Portföljförvaltare och grundare av Coeli Energy Opportunities-fonden.

- Förvaltat aktier inom energisektorn sedan 2006 och har mer än 20 års erfarenhet från portföljförvaltning och aktieanalys.

- Förvaltade fonden Coeli Energy Transition under perioden 2019 - 2023.

- Ansvarig för energiinvesteringarna på Horizon Asset i London under 9 år, en marknadsneutral hedgefond.

- Erfarenhet från energiinvesteringar på MKM Longboat i London och aktieanalys inom teknologisektorn i Frankfurt och Oslo.

- MBA från IESE i Barcelona och Civilekonom från Norges Handelshögskola.

- Innan han började arbeta inom finans var han löjtnant i norska marinen.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.