This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class IUS, other share classes after the fund manager commentary.

FUND MANAGER COMMENTARY

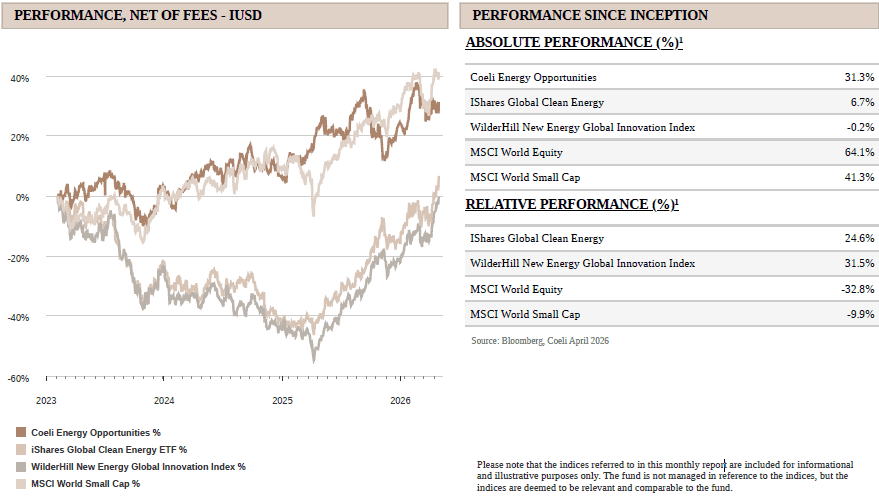

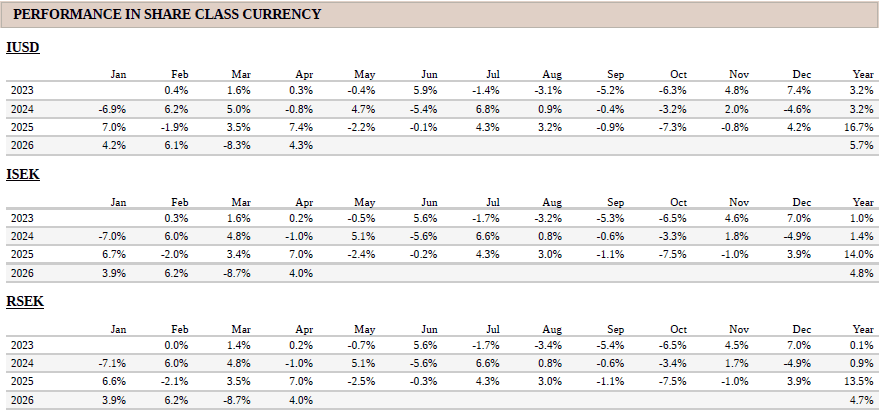

The Coeli Energy Opportunities fund gained 4.3% net of fees and expenses in April (I USD share class). Year-to-date, the fund is up 5.7% and has gained 31.4% since inception in February 2023.

In April, the fund underperformed its most comparable indices, the Wilderhill New Energy Global index (NEX) and the iShares Global Clean Energy (ICLN) by 12.9% and 9.2%, respectively. Year to date, the fund has lagged NEX by 22% and ICLN by 21%, while since inception it remains ahead by 32% and 24%, respectively.

For markets, the AI boom proved the more important force in April, eclipsing the Iran war as the dominant driver of sentiment, particularly after the ceasefire announcement in the second week. Although the Strait of Hormuz remains closed and oil prices rose during the month, the stock market is largely discounting the risk of a prolonged closure and appears to judge, probably correctly for now, that ever‑increasing AI investment more than compensates for higher energy costs. We discuss the latest upgrades to the AI capex cycle later in this report.

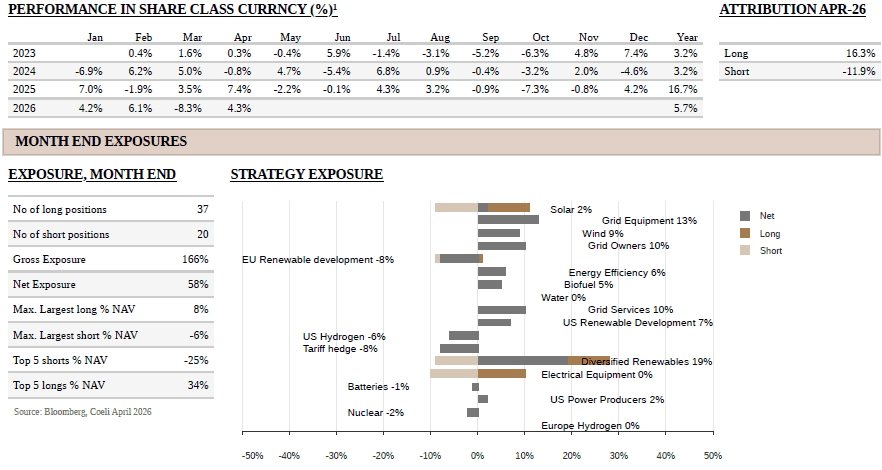

The fund’s long positions returned 16.3% in April, driven by strong performance in themes net long powering AI infrastructure. “Diversified Renewables” added 4.3% to NAV, led by our largest position Siemens Energy (ENR), while smaller positions in Micron (MU), Terawulf (WULF) and HUT 8 (HUT) each contributed almost as much as ENR. “Grid Equipment”, led by Nexans, added 3.3%, and “Grid Services”, led by our second‑largest position Mastec (MTZ), contributed 2.8% to NAV. Offsetting some of these AI‑related gains was a 2.1% loss in “Electrical Equipment”, a net‑short theme that contains several of the hedges for our other AI‑linked themes. In total, the fund lost 11.9% on short positions.

In hindsight, the fund should have had more net exposure to AI themes, particularly into the hyperscalers’ quarterly reports at month‑end. However, the main problem was too many shorts in “concept” stocks that have very little, if anything, to offer AI data centres in reality. Some of these companies are in fact negatively affected by higher power prices, but in the current euphoric market “a rising tide lifts all boats” if you do anything even tangentially related to energy and/or data‑centre construction. “It is only when the tide goes out that you discover who’s been swimming naked”. Since timing that tide is difficult, we reduced these shorts over the month. At month‑end, overall net and gross exposure stood at 58% and 166%, respectively.

MARKET COMMENT – AI ECLIPSES IRAN WAR

The March drawdown was more than recovered for most equity indices in April. The S&P 500 rose 10.4%, while Nasdaq gained 15.6%, its best month since October 2002, when the index bottomed after having fallen more than 80% from the peak of the internet bubble two years earlier. This time is quite different as the index set 10 new all‑time highs in April and has continued to rally into May.

Although the rally is partly driven by euphoric sentiment, systematic flows and “forced buying” by investors wrong‑footed by the Iran war, it is underpinned by a once‑in‑a‑generation capex super‑cycle. AI investment is effectively holding up the US macro picture, more than offsetting the impact of the Iran war and driving strong earnings growth. The first‑quarter earnings season has so far been exceptionally strong, not only with a high beat ratio, but also with a record share of companies beating estimates by more than one standard deviation. Since the start of the year, the full‑year earnings growth rate for the S&P 500 has been revised up by about 4 percentage points to 16%, broadly in line with the index’s 4% year‑to‑date price gain. On 12‑month forward earnings, the index is slightly less expensive today than it was in the second half of last year.

Unfortunately, the earnings trend is not as strong in Europe, which is more affected by higher energy prices and lacks the same AI tailwind as the US. Similarly, US small‑cap earnings for 2026 are down in aggregate since the outbreak of the war. For example, aggregate earnings for the Wilderhill New Energy Global Index, the renewable‑energy benchmark, have fallen by almost 15% for both 2026 and 2027 since the war began, yet the index was up 28% by the end of April. The rising tide really is lifting all boats.

Nevertheless, there are clouds on the horizon. First, the three rate cuts the market expected at the beginning of the year have been replaced by upside risk to rate hikes into next year. Second, the supportive fiscal flows from tax cuts are now behind us. Third, Goldman’s risk‑appetite indicator is at the 99th percentile, versus 34% at the end of March, and both Nasdaq and S&P 500 are in very overbought territory. Fourth, US mid‑term elections are only five months away, and the historical track record for equities into mid‑terms is poor. Finally, despite the ceasefire, the US and Iran are still exchanging fire and the Strait of Hormuz remains closed. Each week that passes with Hormuz shut implies oil prices into next year will be at least USD 3–5 higher, and every sustained USD 10 increase in oil typically knocks around 0.1–0.2 percentage points off US GDP. Soner or later this will affect the broader economy.

Still, as we explain in the thematic section below, this oil‑induced drag on GDP is, at least so far, more than offset by the accelerating AI capex cycle.

AI CAPEX KEEPS MOVING HIGHER - SUPPLY IS THE MAIN CONSTRAINT

Coming into this earnings season, the key question was not whether AI demand was strong. That has been clear for some time. The more important question was whether the reported returns would start to reflect and justify the massive capital investments. Amazon, Meta, Google and Microsoft all reported on the same day and did not disappoint, each delivering strong AI-related revenue growth.

The clearest example was Google Cloud, which grew 63% year on year in the latest quarter, up from 48% and 36% in the two previous quarters. That is not just a high growth rate, it is an acceleration. More importantly, the hyperscalers indicated that revenue growth would have been even stronger if they had had more compute to offer.

The message is clear: They are not short of demand; they are short of compute. That distinction matters. In a typical demand-constrained business, growth is determined by customer appetite. In a supply-constrained business, growth is determined by the speed at which capacity can be added. Once that happens, the bottleneck shifts from software into the physical world: data centres, power availability, grid connections, transformers, switchgear, turbines, cooling systems and construction capacity.

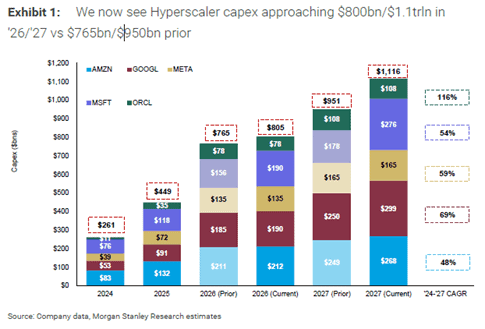

This is also visible in the capex trajectory, the four largest hyperscalers lifted 2026 capex guidance by roughly USD 80bn in aggregate, about 12% higher than forecasts only 3 months ago. Capex for 2026 is now expected to be almost 80% (USD 356bn) higher than in 2025, implying that roughly 1% of US GDP, or close to half the expected GDP growth in 2026, could come from the investments of just four companies.

Similarly for 2027, aggregate capex forecasts for the five hyperscalers have been revised from USD 951bn to USD 1.1tn, close to 3.5% of US GDP. For now, this more than offsets the estimated 0.5%-1.0% drag on US GDP from higher oil prices.

It is not only the need for more compute that is driving the capex bonanza. A big part is cost inflation fuelled by tight supply chains and rising competition for scarce resources. No hyperscaler wants to risk falling behind in what is often framed as a “winners-take-all” market. Usage of AI has strongly migrated toward the best models hence if one player slows spending, it risks losing share quickly. This spending flows directly into the physical layer of the AI economy, where supply chains are slower to respond, lead times are longer and pricing power is often better than in the software layer. This is why we continue to believe that the power and infrastructure enablers remain one of the more attractive ways to gain exposure to the AI investment cycle.

While we are genuinely positive on AI and expect a significant productivity boost, there are several paradoxes.

First, if the hyperscalers are genuinely capacity constrained as demand for compute and tokens are significantly higher than supply, why are prices not rising more aggressively? Most heavy users of AI would agree that the benefits far outweigh the cost, suggesting tokens are currently mispriced.

Management teams might argue it is “too early”, with everyone still in land‑grab mode and AI losses subsidised by legacy profit pools. However, part of the reluctance to raise prices may also reflect intense competition and the fact that switching costs for many AI customers are, for now at least, relatively low.

Second, many argue that hyperscalers are racing toward Artificial General Intelligence (AGI), where the “winner takes all” as self‑improvement loops drive accelerating model performance that competitors cannot match. If that is even partly true, what does that imply for the returns on capital invested by the runners‑up? There might be room for more than one large model, and sub‑AGI systems can still earn attractive returns if they successfully lock customers into their ecosystems. But given the extraordinary scale of investment, the risk of sub‑par returns at the platform level is not trivial.

Third, at a macro level the question is whether AI will generate enough incremental productivity to justify the capital deployed, or whether a large share of the revenue will simply be redistributed from other parts of the economy? Is this a genuine productivity boom, or largely a zero-sum redistribution? We can make arguments for both sides but lean toward considerable productivity gains on a societal level, but with high risk of rising inequality as capital likely takes an even larger share of total income. On the other hand, as multiple credible competitors build similar capabilities and durable competitive advantages remain elusive, we could end up with an outcome similar to past investment booms, where much of the productivity gain is ultimately socialised rather than captured by shareholders.

We are clearly living through an unusual moment, and it will take years before we know how these tensions ultimately resolve. What does seem evident today is that the AI power and infrastructure investment boom is even stronger and more durable than we assumed for most of last year and into this year. There are physical limits to how long AI capex can grow at 70% per year, or even 30–50%, but the set‑up for companies supplying AI power and infrastructure continues to improve as the cycle extends and the bottlenecks become increasingly physical rather than digital.

In that sense, the key point is not the exact capex number for any given year, but the direction of travel. Estimates for AI-related infrastructure spending keep rising, especially into 2027. The arms race is still accelerating, and for our universe the binding constraint remains unchanged: the world can write software faster than it can build the power systems, grids and data centre infrastructure needed to run it.

FUND PERFORMANCE - POWERING AI DOMINATING PERFORMANCE

April was another challenging month for the fund. Despite a net return of 4.3%, with 70% of themes making gains and long positions adding 16.3% to NAV, overall net exposure to AI was not high enough, and several short positions were squeezed as retail hype spread across AI and renewable‑energy names.

The best‑performing themes were all AI‑related. “Diversified Renewables” contributed 4.3% to NAV, led by Siemens Energy (ENR) but with substantial contributions also from memory‑chip company Micron (MU) and “bitcoin miners” Terawulf (WULF) and HUT 8 (HUT). We first wrote about MU in our annual report in December, after initiating the position in September last year. While memory‑chip manufacturers are not a typical focus area for the fund, we identified early that memory would be one of the most critical bottlenecks in the AI supply chain. Despite the share price having more than doubled so far this year, the stock still trades on around 7x 2027 earnings. Historically, this has been a classic boom‑and‑bust industry in which high prices destroy demand and margins collapse when new capacity arrives. That will inevitably happen again, but whereas the end customer in a “normal” cycle is a price‑sensitive PC or mobile‑phone buyer, the marginal buyer today is a price‑insensitive hyperscaler in urgent need of more compute and tokens. Given the sharp recent increases in hyperscaler capex, we do not expect memory pricing to collapse any time soon.

Another industry we identified while searching for AI bottlenecks was the so‑called bitcoin miners. We first invested in and wrote about this space in our November 2024 report, “The Urgency to Secure Power”. At that time, the miners typically owned large sites with high‑quality grid connections and long‑term clean‑power contracts that could be repurposed relatively easily into high‑performance computing (HPC) data‑centre capacity. Today, it is almost unfair to call these companies bitcoin miners as they have transformed into HPC infrastructure providers offering large‑scale, often low‑carbon, power capacity to AI tenants. The stocks have performed extremely well, and with the urgency around time‑to‑power only increasing, we remain constructive on the group.

The theme “Grid Equipment”, which added 3.3% to NAV in April, is long European companies supplying equipment to build and reinforce the electricity grid. While they benefit from “Powering AI”, we have been positive on this space since well before ChatGPT’s launch in late 2022. AI is, in many ways, just ‘the icing on the cake’ for companies already leveraged to electrification, distributed generation and structurally rising power demand. Although valuations are clearly more demanding than three to four years ago, we remain optimistic as order backlogs continue to grow.

A related theme is “Grid Services”, which contributed 2.8% to NAV in April. This theme is net long US EPCs that provide engineering and construction services for large infrastructure projects across energy, communications and oil and gas. Names like Mastec (MTZ) and Quanta (PWR) have been in the portfolio for years and have performed exceptionally well. We have long been wary of multiple expansion, but demand for their services is now “through the roof”, and it is increasingly obvious that skilled labour is one of the main bottlenecks in the AI build‑out. We believe these companies enjoy significant pricing power in the current scramble to build power and infrastructure for AI data centres.

We are still hedging AI risk with positions in electrical‑components manufacturers that, in our view, despite running close to full capacity have limited pricing power as competition is intense. These hedges have mostly worked well, although some names have become crowded shorts and are not working in the current euphoric environment. We have reduced these positions, along with cuts to shorts in green hydrogen, fuel cells and nuclear. The fact that the stock market has priced out three FED rate cuts since the outbreak of the Iran war, and that the next move in rates is as likely to be up as down, should weigh on companies whose positive cash flows lie far in the future, if they materialise at all. However, in the current ecstatic market environment we have chosen to reduce these shorts, recognising that the seemingly never‑ending rise in AI capex could push such stocks to even more stretched valuations.

From a positioning perspective, we therefore remain structurally long the power and infrastructure enablers of AI, grid equipment, grid services, diversified renewables and selected “HPC infrastructure” names, while keeping a more selective, tactical approach to shorting the weaker parts of the energy‑transition and AI ecosystem. Our focus is on businesses with tangible assets, strong order books and clear pricing power, balanced by a smaller but active hedge book designed to protect the portfolio if the current AI euphoria eventually gives way to a more discriminating market for capital.

Thank you for your continued trust and confidence. We look forward to updating you again next month.

Sincerely

Vidar Kalvoy & Joel Etzler

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

- Portföljförvaltare och grundare av fonden Coeli Energy Opportunities.

- Mer än 15 års erfarenhet av investeringar från både publika och private equity-sidan.

- Förvaltade fonden Coeli Energy Transition under perioden 2019 - 2023.

- Spenderade sex år på Horizon Asset i London, en marknadsneutral hedgefond.

- Började arbeta tillsammans med Vidar Kalvoy 2012.

- Fem år inom Private Equity på Morgan Stanley.

- Startade sin investeringskarriär inom tekniksektorn på Sweden Robur i Stockholm 2006.

- Utbildad Civilingenjör från Kungliga Tekniska Högskolan.

- Portföljförvaltare och grundare av Coeli Energy Opportunities-fonden.

- Förvaltat aktier inom energisektorn sedan 2006 och har mer än 20 års erfarenhet från portföljförvaltning och aktieanalys.

- Förvaltade fonden Coeli Energy Transition under perioden 2019 - 2023.

- Ansvarig för energiinvesteringarna på Horizon Asset i London under 9 år, en marknadsneutral hedgefond.

- Erfarenhet från energiinvesteringar på MKM Longboat i London och aktieanalys inom teknologisektorn i Frankfurt och Oslo.

- MBA från IESE i Barcelona och Civilekonom från Norges Handelshögskola.

- Innan han började arbeta inom finans var han löjtnant i norska marinen.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.se/finansiell-och-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.