“It feels like a bubble to me.” - Jeff Bezos, September 2025

To be clear, Jeff Bezos is not claiming that AI technology lacks substance or long-term value. In fact, he believes AI is authentic, ‘going to change every industry’, and will deliver ‘gigantic benefits’ to society over time. However, he argues that AI is experiencing an ‘industrial bubble’ driven by investor exuberance and draws parallels to the investment frenzy of the IT-bubble.

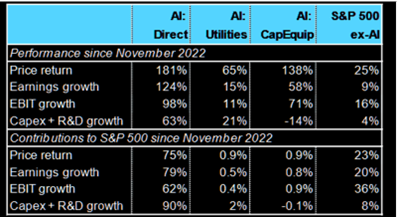

Let’s examine the facts. J.P. Morgan reports that since the launch of ChatGPT in late 2022, AI related stocks have contributed roughly 75% of S&P 500 returns, 80% of earnings growth, and 90% of capital spending.

Comparison to the IT-bubble

AI is undeniably a major force in the stock market, but is the comparison to the IT bubble justified? Possibly.

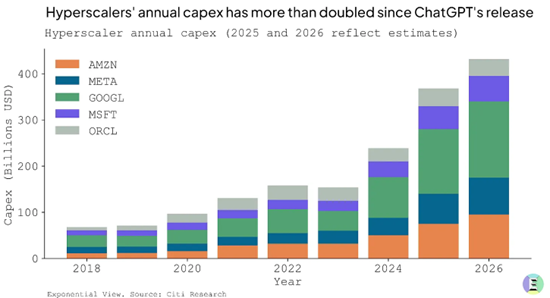

First, a key metric to monitor is hyperscaler capital expenditures. The five largest technology companies are set to spend nearly USD 400bn on AI data centres in 2025, representing an increase of approximately 60% over last year. Strikingly, according to Harvard economist Jason Furman, US GDP growth would have been just 0.1% in the first half of 2025 without investment in “information processing equipment and software”. This segment alone, where hyperscalers account for a large share, was responsible for 92% of GDP growth during that period. Forecasts for the top five tech companies’ capex indicate an additional 15-20% growth in 2026. Since previous projections have consistently underestimated spending, and with data centre announcements accelerating in recent months, these figures could ultimately be even higher.

Is this level of spending excessive? It is uncertain, but unlike during the IT bubble, the investments today are financed by the world’s largest and best-capitalized corporations. These companies can literally ‘afford’ to burn some hundreds of billions of dollars in the pursuit of Artificial General Intelligence (AGI).

Second, can it truly be a bubble when demand for compute power vastly exceeds supply? During the fibre optic build-out of the late 1990s and early 2000s, only a fraction of the installed capacity was utilized after the bubble burst in 2000-2001. Today, data centres cannot be built quickly enough to meet demand. For example, Oracle (ORCL) recently reported Remaining Performance Obligations (RPOs), i.e. revenue booked but not yet recognized, of USD 455bn, up 359% year-on-year, a staggering acceleration compared to 41% growth in the previous quarter. Supply simply cannot keep up with demand, at least not yet. Importantly, the limiting factor is not just computer chips but increasingly long-term access to power, as highlighted in our March-24 report “Roadblocks on the AI highway” and reiterated this summer by former Google CEO Eric Schmidt. Given the time and complexity involved in generating large amounts of new energy, compute power may remain in short supply for some time.

There are other distinct differences from the IT bubble. Hyperscalers now bear a large portion of the investment burden, boasting robust balance sheets, solid earnings and strong cash flows. While their market capitalizations are in the trillions, their valuations are generally reasonable considering projected earnings growth.

Concentration risk is excessive

However, the concentration risk for equity investors is greater than ever. The ten largest stocks, which are all technology companies, now comprise 39% of the S&P 500, which itself represents over half of global equity markets, meaning these ten tech companies account for roughly 20% of total global market capitalization. This concentration is striking and clearly amplifies systemic risk, making any weakness in AI a risk to investment portfolios worldwide.

Is a bubble brewing?

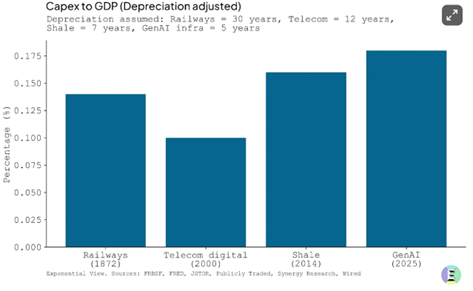

What is the likelihood that spending on AI data centres is excessive, blowing up a bubble? The odds are not insignificant. Comparing the current AI build-out to historical booms like the railway mania of the 1800s and the IT-bubble of the 1990s, AI capital expenditures relative to GDP already surpass those earlier booms.

Overbuilt infrastructure is historically rather a feature, not a bug of transformative infrastructure spending cycles. Despite severe investor losses in past booms, society reaped lasting benefits. One concern, though, is that most AI investment flows into data centres, where about 60% of the costs consist of fast-depreciating GPUs. This implies that much of the invested capital dissipates quickly, unlike railways and fibre networks, which continued to benefit society long after the initial bust.

Signs of financial engineering are emerging. While not yet matching the scale seen during the IT-bubble, these developments are nonetheless noteworthy. First, hyperscalers have quietly extended GPU depreciation schedules, from 3–4 years in 2020–21 to 5–6 years now, stretching costs over a longer period and boosting reported earnings. This adjustment has played a significant role in their consistent earnings beats. Hyperscalers justify the change by claiming that, as we transition into the age of inference, the useful life of GPUs is extended as these depreciated advanced GPUs for learning models can be repurposed for inference. However, this rationale remains highly uncertain, especially as Nvidia moves to near-annual upgrade cycles, rendering such accounting adjustments increasingly questionable amid a heightened investment boom.

Second, innovative off-balance-sheet financing is being used to fund data centres. For example, Meta’s latest data centre (USD 29bn) is leased from a Special Purpose Vehicle (SPV) owned by private credit infrastructure funds charging 200–300 basis points more than Meta could have secured with traditional on-balance-sheet debt. While this structure keeps liabilities off Meta’s balance sheet, it also disperses risks beyond the company itself, potentially to society at large.

Third, vendor financing is back. Nvidia’s recent pledge to invest USD 100bn in OpenAI through a vendor-financing arrangement is reminiscent of late-1990s telecom excesses. OpenAI has even confirmed that much of the funds will return to Nvidia. Maybe more concerning is OpenAI partnership with AMD to deploy chips for up to USD 100bn paid for by AMD granting OpenAI warrants that can be monetized as milestones are reached. Such circular financing did not end well a quarter-century ago when the IT- bubble burst.

Ultimately, these are only signs of a potential bubble. As with the IT-bubble, the crucial test for AI investments will be their returns. The internet bubble burst when market focus shifted from spending to realized profits. For AI, equity markets are still in the “easy” phase: the more spending is promised, the higher revenues and profits are extrapolated, driving share prices upward. However, attention will soon turn to actual AI revenues and ROI, and disappointing results could abruptly end the rally.

AI is the key macro driver

AI is now the most important macro driver for equity markets. While AI is poised to have a transformative impact and improve productivity, it remains uncertain whether the returns will benefit investors broadly or be socialized, as in many previous investment booms. Regardless, like all asset booms, there will be winners and many losers, providing abundant opportunities for long-short hedge funds that can ride the winners and also profit from a potential decline when ‘there is nowhere else to hide’.

- Portföljförvaltare och grundare av fonden Coeli Energy Opportunities.

- Mer än 15 års erfarenhet av investeringar från både publika och private equity-sidan.

- Förvaltade fonden Coeli Energy Transition under perioden 2019 - 2023.

- Spenderade sex år på Horizon Asset i London, en marknadsneutral hedgefond.

- Började arbeta tillsammans med Vidar Kalvoy 2012.

- Fem år inom Private Equity på Morgan Stanley.

- Startade sin investeringskarriär inom tekniksektorn på Sweden Robur i Stockholm 2006.

- Utbildad Civilingenjör från Kungliga Tekniska Högskolan.

- Portföljförvaltare och grundare av Coeli Energy Opportunities-fonden.

- Förvaltat aktier inom energisektorn sedan 2006 och har mer än 20 års erfarenhet från portföljförvaltning och aktieanalys.

- Förvaltade fonden Coeli Energy Transition under perioden 2019 - 2023.

- Ansvarig för energiinvesteringarna på Horizon Asset i London under 9 år, en marknadsneutral hedgefond.

- Erfarenhet från energiinvesteringar på MKM Longboat i London och aktieanalys inom teknologisektorn i Frankfurt och Oslo.

- MBA från IESE i Barcelona och Civilekonom från Norges Handelshögskola.

- Innan han började arbeta inom finans var han löjtnant i norska marinen.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.