We would argue no, not even close. So, if we are using the wrong metrics, how come climate investments are so high on the agenda for sustainable funds and why are so many subscribing to being net zero by 2050?

The conventional wisdom is to measure companies’ Scope 1-3 emissions and to invest in those with low emissions or a credible plan to reduce them. In many cases, Scope 3 emissions are the largest and most relevant, yet because they are difficult to measure, they are often excluded from calculations.

Is there any point to even consider emissions if you cannot accurately measure scope 1, 2 and 3 emissions? Yes and no. One the one hand, mathematically it makes no sense. It is like judging the performance of a fund that only reports profitable trades or only trades in one of its regions. Aggregating this at a portfolio level makes even less sense since one company’s Scope 2 emissions are another’s Scope 1, the risk of double counting is significant. We are now at a mathematical sanity level close to measuring only the positive trades in the US for a global equity fund, essentially meaningless.

On the other hand, investors’ focus on emissions influences companies to attempt measuring them, which is after all a pre-requisite to actually reducing their footprint. Moreover, data is constantly improving and with time, these metrics should become more useful.

Nevertheless, let us not lose sight over what is the purpose of the reporting. No, it is not to line the pockets of ESG consultants, though it sometimes feels that way. The real goal is, or should be, to channel capital toward companies that are actively contributing to a greener world and leading us toward net zero.

So, which companies are providing the products and services that will get us to net zero? Renewable energy companies are the clearest example. Their products may generate emissions upfront, but over time, they lead to substantially lower overall emissions. Renewable energy is one of the few viable solutions for the world to reduce total emissions.

However, renewable energy companies, for instance those involved in solar, wind, batteries, hydro power and even nuclear, have relatively high emissions during construction and consequently generally score worse on Scope 1-3 than companies with business models that does not involve power generation. Given that about three-quarters of all global emissions stem from human’s use of energy, it is perplexing that clean energy is given a worse emission score than companies selling for instance software or banking services. The current measure simply does not give credit for the avoided emissions. This is where Scope 4 comes in—a metric that could make emission reporting far more useful by recognizing the avoided emissions and the real contribution companies make toward a low-carbon future. We discussed the background of the work we have done on Scope 4 in our February 2024 monthly report “HOW CAN YOU TELL IF A FUND IS GREEN?”

We also described that there are different classifications of funds with article 9 funds being the most sustainable, according to the Sustainable Finance Disclosure Regulation (SFDR). To be an article 9 fund, the investments shall be sustainable first and performance focused second.

It is therefore noteworthy that two of the most well owned companies by article 9 funds are two of the world’s largest companies, Nvidia and Microsoft, both have around 200 article 9 funds on the list of shareholders, according to Bloomberg.

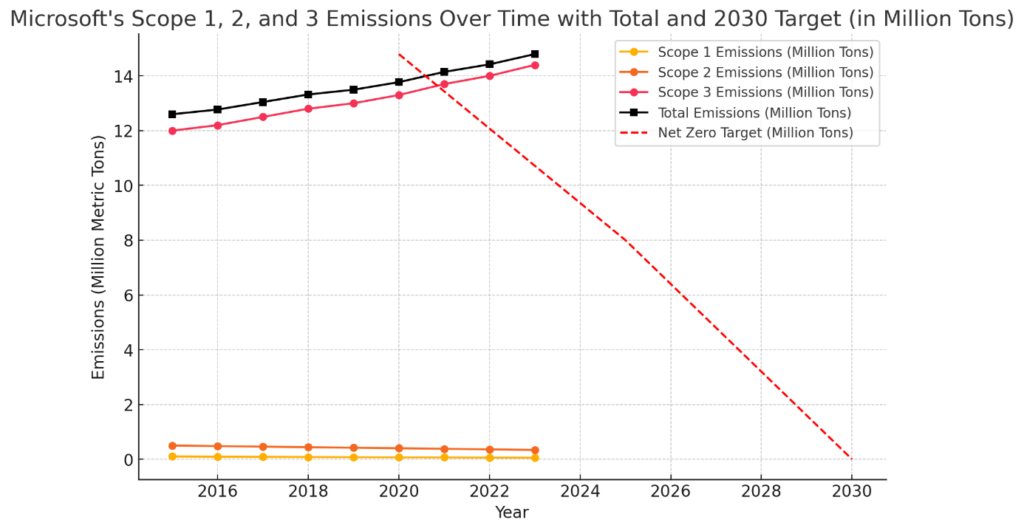

Let us take a closer look at Microsoft. Despite its gigantic size, not only does it have the resources to be able to report ESG in a very detailed manner, but it also has very ambitious climate goals. In fact, in 2020 it released its moonshot plan of net zero by 2030, which means that by 2023 it should have reduced emissions by 30%. Instead, it has increased emissions by as much as 30% so far.

Microsoft 2024 sustainability report, ChatGPT

To be fair, the short fall is not due to Microsoft’s lack of effort and capital invested in decarbonisation, it is rather a consequence of accelerated build out of power-hungry and very profitable AI Datacentres. Clearly, Microsoft, with a fiduciary duty to its shareholders, has prioritized profit over climate, but how does that square with the goal of article 9 funds to be sustainable first and performance focused second?

We believe it is evident that new and improved systems of measurement are required for the investment management industry to be able to claim to do “green” investments that can be confirmed by objective metrics.

To that end, as described in our February 24 report, we have collaborated with researchers at Linköpings University in Sweden to develop a method to calculate and allocate Scope 4 emission across the value chain. Although initially focused on solar and wind applications, the method can also be applied to adjacent and important sectors like power grids. We believe this is crucial in understanding what investments really make a difference for the climate.

We encourage you to take a look at the report:

https://liu.diva-portal.org/smash/record.jsf?pid=diva2%3A1880366&dswid=-4215

A key aspect of the research pertains to the Life Cycle Analysis (LCA) and the allocation of the emissions between different products. This allows the benefit of avoided emissions to not only be attributed to the wind turbine or solar panel manufacturer but to be shared with equally critical products and services like grid power lines, transformers or wind installation vessels. The LCA allocates the avoided emissions based on the physical relationship between the products or as can be seen in the report, the monetary value the products bring to the process.

Currently the electrical grid for instance, a key enabler of electrification, would without a robust LCA not get credit for the emissions it helps to avoid. As an example, the fund owns electricity distributor EON (EOAN), which has relatively high Scope 1-3 emissions and its activities are only 19% EU taxonomy-aligned according to its latest filing. It does not screen as a particularly sustainable investment. However, the company will be investing EUR 34bn over the next 3-4 years in the power grid, coincidentally the same as its market value. Without these investments, it would be difficult to add new renewables to grid and the electricity generated by new solar and wind plants would not reach Microsoft’s new data centres.

The work on Scope 4 is unfinished and needs to continue with further refinement. We believe it is a good start as it is focused on the two fastest growing energy sources globally. This makes it instantly useful, and we do hope that this work will lead to further research and development in this field. Asset managers are in dire need of more useful data that incentivises the allocation of resources to companies that help the world reduce emissions, not just grow them at a slower rate.

If you are interested in more information, please reach out.

- Portföljförvaltare och grundare av fonden Coeli Energy Opportunities.

- Mer än 15 års erfarenhet av investeringar från både publika och private equity-sidan.

- Förvaltade fonden Coeli Energy Transition under perioden 2019 - 2023.

- Spenderade sex år på Horizon Asset i London, en marknadsneutral hedgefond.

- Började arbeta tillsammans med Vidar Kalvoy 2012.

- Fem år inom Private Equity på Morgan Stanley.

- Startade sin investeringskarriär inom tekniksektorn på Sweden Robur i Stockholm 2006.

- Utbildad Civilingenjör från Kungliga Tekniska Högskolan.

- Portföljförvaltare och grundare av Coeli Energy Opportunities-fonden.

- Förvaltat aktier inom energisektorn sedan 2006 och har mer än 20 års erfarenhet från portföljförvaltning och aktieanalys.

- Förvaltade fonden Coeli Energy Transition under perioden 2019 - 2023.

- Ansvarig för energiinvesteringarna på Horizon Asset i London under 9 år, en marknadsneutral hedgefond.

- Erfarenhet från energiinvesteringar på MKM Longboat i London och aktieanalys inom teknologisektorn i Frankfurt och Oslo.

- MBA från IESE i Barcelona och Civilekonom från Norges Handelshögskola.

- Innan han började arbeta inom finans var han löjtnant i norska marinen.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.